New Tax Rules - Residential Landlords Are Winners

Checking on Accuracy of My Crystal Ball

In January of this year, I predicted that 2018 will be the year of promise for landlords. My core belief was, based on the facts that:

- Employment & Wages Are Up;

- Taxes Are Down; plus a

- Brand New, Major Tax Break for Residential Rental Investors

Click Here for the full article. As we approach the end of the third quarter of 2018, the above still points to “all good” news for Virginia residential rental investors! In this issue, see it from a property manager's point of view on how these new tax rules are benefiting residential rental investors … now that we have some history of the application of the new tax law including guidance and interpretations by the IRS.

How the Tax Cuts and Jobs Act (TCJA) Affects Landlords

First off, let me be clear. I am not a professional when it comes to interpreting tax law. That said, you are urged to meet with your tax advisor and seek professional guidance for the specifics of TCJA as it may apply to your unique circumstances. Here, I only present my understanding of the provisions of the revised Act and how I think it presents unique advantages to residential rental investors.

New Pass-Through Tax Deduction The vast majority of residential rental landlords own their properties as sole proprietors, partnerships or S corporations … all deemed pass-through businesses. That means profits earned from rental activity is passed through to the owner(s) to pay tax at their individual tax rates. Profits are net of allowable deductions for such things as mortgage interest, state and local real estate taxes, utilities, insurance, repairs and maintenance, yard care and association fees.

The TCJA changes that in two dramatic ways.

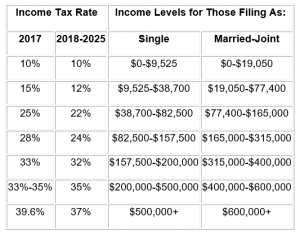

First, the Act retains the seven income tax brackets of the previous tax code, but with reduced tax rates for individuals in all brackets but one. That means tax-savings for taxpayers with pass-through income, including profits from residential rental properties. Comparison of New Tax Rates vs. Old

Note: Capital gains rates remain unchanged under the new law. Second, the TCJA permits a tax deduction of up to 20 percent of business related income with some limits and exceptions. Most rental activity qualifies, for tax purposes, as a business. That means landlords may deduct 20% of net rental income over and above all other rental-related deductions. Net result … only 80% of rental income will be taxed. This could be HUGE!

There are income qualifications. Your total taxable income for the year must not exceed certain limits … $157,500 for a single-filer, or $315,000 for a married couple filing jointly. If your income exceeds these limits, the amount of the deduction begins to diminish, disappearing altogether for single filers with income above $207,500 or a married couple filing jointly with income above $415,000.

Even if your income exceeds the amounts listed above, you can still benefit from the change in the law. It’s best to seek guidance from your tax advisor as the qualifications are a bit complex. Note: This deduction is effective in tax year 2018 and remains in effect until January 1, 2026 … a "sunset" provision that affects many aspects of the new tax law.

Section 179 Deductions This section of the tax code has never applied to rental property owners. Now, under the TCJA, residential rental owners are permitted to deduct in one year the cost of depreciable personal property used in the rental business. Personal property includes furniture and appliances and perhaps carpeting and flooring and other equipment used in the living quarters of a lodging facility such as an apartment house, dormitory, or other facility where sleeping accommodations are rented out. Beginning in 2018, the maximum annual deduction is $1 million, up from $510,000 in 2017,that may now be deducted in one year rather than amortizing eligible expenses over several years.

This is a major victory for residential rental landlords!

Note: Section 179 deductions cannot create or increase an overall tax loss from business activities. Your tax adviser can help you assess this issue based on your business taxable income. Self Employment Taxes As business owners, landlords are required to pay Social Security and Medicare taxes on their net business income in addition to income taxes. These taxes are called self-employment taxes. Under the TCJA landlords who do not provide substantial personal services to their tenants (e.g. a bed & breakfast or hotel) are now exempt from having to pay self employment taxes. That means savings of 12.4 percent on your Social Security tax and 2.9 percent on Medicare taxes.

Summary

There are additional provisions, but the above is my understanding of the significant, positive affects the new tax law delivers for residential rental investors. The National Association of Realtors (NAR) has an interesting take on tax reform. NAR said it would be much more advantageous to rent a house than to buy one based on the new rules.

While savings with the new tax bill will vary based on earnings, the NAR believes just about everyone will save more money in taxes by renting. Lots going on in the Richmond /Tidewater residential rental markets … most of it positive and upbeat. That coupled with the benefits to landlords under the Tax Cuts and Jobs Act points to robust opportunities for investors for the balance of this year and into 2019.